Nothing new here; just more evidence that forecasting interest rates is very hard. Info from the Wall Street Journal… Not one economist surveyed predicted that 10-year interest rates would be as low as they are now!

Whither Rates Up or Down?

Forecasting the path of interest rates is very hard; impossible, really. That doesn’t stop talking heads from trying to do it. Starting in the post-Credit Crisis environment of 2008/2009, most thoughts pointed to rampaging inflation and sky-rocketing interest rates in the aftermath of aggressive Fed easing and increases in the money supply. Certainly, that has not been the case.

Interest rates and inflation continues to be muted and well under control. The 10-year treasury is currently yielding 2.13% today and from 2009 to today has been within a range of 3.98% (April 2010) and 1.38% (July 2016); a small range with hardly a trend. Fed Funds, on the other hand, has moved up in a telegraphed and orderly manner from about 0% from 2009 to 2016 and then up in steps to about 2.37% today.

Barron’s had a few articles on interest rates in the June 10, 2019 issue. One article titled, “Say Goodbye to Those 2% Rates on Savings”, made a point that Wall Street thinks interest rates are going lower. So, if you have that view, some strategies that could benefit could include to try to lock in rates, place some bets on financials (that might be more profitable in a steep yield curve environment), or buy real estate investment trusts that could broadly benefit from a general decrease in rates.

Another article titled, “The Rate Swing of a Generation” by rate guru James Grant, made the point that bonds have traded in two great long-lived markets: the bear market of 1946-1981 and the bull market from 1981-2016 (which may be extended if we get another round of rate cuts). He is not forecasting anything; instead, he is positing that rates could rise from here. He thinks we have an unreasonable “love” for bonds that could turn on us. One point he makes is that “real” rates, rates after adjusting for inflation, are historically low and should not persist.

So, no one knows and there are plenty of differing views. Undiversified bets in either camp could cost you; best to stay diversified.

More Trouble with Tactical: GMOM Update

I have reported a few times in this space about the difficulty tactical managers have had in the recent market environment. This update today continues to show a trend of underperformance.

In February, the Cambria Global Momentum ETF (ticker: GMOM), a notable player in the tactical space, called a risk-off environment. As of June 4, 2019 the ETF is comprised of almost 100% bonds (of different varieties and flavors) and no equities except for some REIT exposure. Year-to-date through June 4, 2019, the ETF has produced a total return of 2.71%, compared to the S&P 500 of 12.74% and the Bloomberg Barclays U.S. Bond index of 4.91%. Most interestingly, yesterday June 4 when the S&P 500 was up 2.2%, this fund was up only 0.4%. Unremarkable performance by any measure.

This market environment has been characterized by geo-political turmoil, trade battles, Fed-speak, and economic stats that present a mixed bag of conclusions. More can be said on this topic, but let it be known that trying to outguess this market is ripe with risk. For long-term investors who have correctly evaluated their tolerance for risk, it is best to stay the course.

May PMI at 52.1

Weakening trends continue in the important ISM Purchasing Managers Index (PMI) manufacturing stat. April PMI was 52.8 that declined to 52.1 in May. This aspect of the U.S. economy is still growing, but at a slower pace than any time since October 2016. Under 50 indicates a contraction in manufacturing.

So, though there are many negative signs in the economy, offset by some positive signs, there is little indication for a prolonged drawdown. For long term strategic accounts, I see good reason to be cautious, but no reason to be tactical and reduce exposures in risky assets at this time. Active accounts with a tactical bias may be inclined to take risk off as a bet.

Here We Go Again

The yield curve inversion has reared its ugly head again with the typical market jitters, but this time it is accompanied by a few “friends” that could prompt concern. As of today, the 3-month/10-year spread has a solidly negative relationship at 2.36% to 2.25%, respectively. This alone is not too notable, despite what some of the “talking heads” may lead you to think. I am skeptical of the research on this point since I think there are too many behavioral biases, externalities and other variables to effectively model causation. But, when it is accompanied by other stats pointing in the same direction I take notice.

What is worrisome about it this time? For the first time since 2016 Q4, the April ISM Purchasing Managers Index (PMI) has grown at its slowest level. I am a fan of the PMI and the May PMI is due on Monday, June 3. A continuation of this trend could be troublesome. It could very well be a short term blip, but it is continuing a softening trend we have seen since March. China, Mexico and Brexit pop up as the chief culprits influencing the stats; we are hopeful that market forces will help correct any imbalances, but it could take a while to adjust.

Another stat to take note of is the Conference Board Leading Economic Indicators (LEI). It continued to show increases for February, March and April, but could be setting up for a surprise in May. This stat covers many different aspects of the economy, including the impact of stock prices that could push the index down.

Market momentum has eased in May after a strong rally through April. A few technical barriers have been crossed, but we are still (just barely) over the 200-day moving average. A continuation of this trend is worrisome.

Thankfully, all is not lost! For one, the yield curve inversion is occurring with a general decline in rates. U.S. Treasury bonds are a safe haven investment around the globe, so when there are geopolitical hiccups, it is logical that U.S. Treasuries get bid up in a “flight to quality.” It certainly doesn’t hurt demand for U.S. treasuries that “negative” yielding sovereign debt still persists in large numbers around the Eurozone and elsewhere. Also, corporate and high yield bond spreads have weakened a bit in May but continue to get a bid, so stable bond markets give comfort that we are not entering a crisis stage.

Beat the Benchmark

Long term strategic investing is usually baselined against naïve mixes of the S&P 500, as a proxy for a broad mix of large cap U.S. stocks, and the Bloomberg Barclays U.S. Aggregate Bond Index (AGG), as a proxy for broad core bonds including U.S. government and investment grade corporate bonds. These broad naïve categories, however, miss many areas of the capital markets and optimized asset weighting that could provide extra diversification and additional return per unit of risk.

So far during 2019, some of the passive exchange-traded funds (ETFs) that are designed to track a broader selection and optimized mix of assets have added incremental return to naïve mixes of the S&P 500 and AGG.

Two equity ETFs that have done well are the iShares Edge MSCI Min Vol USA (USMV) and the iShares Edge MSCI USA Momentum Factor (MTUM). Both of these ETFs are structured to capture some of the “factor” anomalies that research has shown to outperform the naïve S&P over time. YTD through May 24, USMV and MTUM have returned 14.93% and 14.06%, respectively, whereas the S&P 500 (SPY) has returned 13.64%.

Real estate investment trusts (REITs) are a good asset class to help diversify equity exposures and also hedge against inflation. An ETF that tracks that asset class is the Schwab US REIT ETF (SCHH). Real Estate Investment Trusts tend to be a more risky subset of the equity space and has returned 17.26% so far in 2019, beating the 13.64% of the S&P 500.

Another innovative ETF that helps diversify exposure is the AI Powered Equity ETF (AIEQ). This ETF uses artificial intelligence in the portfolio management process with a target to outperform the S&P 500 with a similar amount of risk. Year-to-date through May 24 this ETF has returned 17.74%, easily outpacing the 13.64% of SPY.

Likewise, selected carveouts of the fixed income space have easily beat the Bloomberg Barclay Aggregate U.S. Bond index (AGG). While the AGG has returned 3.76% YTD, other fixed income sub classes have added incremental return and diversified exposures. For example, preferred stocks (represented by iShares Preferred & Income Securities ETF, PFF) has returned 9.03%. Additionally, the high yield bond, investment grade corporate bond, emerging market bonds, and bank loans (tracked by HYG, LQD, EMB, and BKLN) have all outperformed AGG with 7.49%, 7.42%, 7.10%, and 6.44% respectively, against the AGG of 3.76%.

In this environment, a broader diversification approach and optimized weighting will help portfolios to outperform the naïve S&P 500 and the AGG.

That's Life!

“You're riding high in April

Shot down in May

But I know I'm gonna change that tune

When I'm back on top, back on top in June”

- Frank Sinatra

Not sure if Frank Sinatra was thinking about the stock market when he sang those words back in 1966, but they certainly seem apropos! Through April 2019, the S&P 500 was up 18.3% year-to-date; in May alone, the index has given back 4.6% so far though May 13!

On last Friday, the U.S. increased trade tariffs from 10% to 25% on $200 billion of Chinese goods. China then retaliated announcing an increase of tariffs on $60 billion of goods. Prior to this, the markets had accepted that trade negotiations were proceeding smoothly. Words like “constructive” and “candid” were tossed around like candy to children to appease anxious markets.

As of now, economists are producing all kinds of statistics to measure the economic and earnings impact this may have on the U.S. or global markets; they are all over the place! Not surprisingly, all the forecasts are negative, thus the negative market reaction.

However, these forecasts presume that the tariffs persist, increase, and never get resolved. No one knows, of course. But, I have faith in the market system and believe that whatever happens will end with a positive outcome for all parties; as in all good negotiations. What we are seeing here is a knee jerk reaction to the unknown. It is reasonable to be cautious, but the market could just as easily knee jerk in the other direction once this gets resolved - since it will; hopefully producing winners on both sides!

It takes a lot to produce a large market drawdown; this alone is not it – yet. We will continue to watch.

The “New” New Normal?

Are we in or entering a “New” New Normal? It is still a developing story, but the persistent short rotations into and out of high and low volatility periods, more stable economic growth with less severe peaks and troughs, trending lower unemployment with surprisingly low income growth, and growing corporate earnings all point to a new paradigm that capital markets are embracing. The latest indicators show a continuation of these trends.

The first business day of every month is a big day for capital markets because that is when the ISM PMI (Institute for Supply Management Purchasing Managers Index) report is released. This May 1 report for April continued a trend that started 10 years ago; for the 120th straight month the ISM PMI index indicated a GROWING economy! The index reading showed a value of 52.8 for April (readings over 50 indicate a growing manufacturing sector).

This is one of the most important economic indicators that I follow. Combining this with other indicators like leading economic indicators (LEI), industrial production, job and income growth, yield curve, technicals, asset correlations, etc. can give a good measure of how we are doing and if things are getting unhinged.

Year-to-date through May 3, market strength seems well-deserved. As I reported back on December 31, 2018, “On balance, there are warning signs, but no reason yet to run for the hills. The recent stock sell-off [during Q4 2018] has priced equities attractively and corporate bond spreads are reacting favorably with spreads lower than recent historic (indicating less concern about default risk).”

History tends to repeat itself, so let’s not get ahead of ourselves. But, for now, let’s enjoy the ride!

The Benefits of AI Portfolio Management

The first exchange-traded fund (ETF) to be managed by artificial intelligence, AI Powered Equity ETF (AIEQ) was launched with a bit of fanfare back in October 2017. After all, it used the ground-breaking (and Jeopardy-beating) logic of IBM’s Watson Artificial Intelligence to manage the stock selection and portfolio management function. Asset growth started slow, then jumped to over $100 million in 2018 and it currently resides close to the $150 million range.

The benefit to the investor of this ETF is its active strategy that is insulated from behavioral biases and scours all financial and unstructured (news articles) information as the portfolio management approach. Its investment goal is to outperform the broad equity market (investing in all market capitalization sectors) at a similar level of risk. In theory, it should provide a good low-correlated complement to an index-based approach to portfolio management.

Performance since inception has been mixed. It has rotated from lagging, then matching, then beating (by a lot!), then lagging again (by a lot!), while now recently beating the S&P 500. From inception through April 5, 2019, AIEQ is up +15.4% compared to SPY being up +16.4%. On a YTD basis through April 5, 2019, AIEQ is way ahead at +21.46% compared to S&P 500 at +16.02%; ranked in the highest 2 percentile in its Morningstar Large Blend Category.

It is too early to evaluate how well AIEQ has performed as a portfolio complement, but it has certainly provided a strong case for it to remain as a portfolio position. Unlike tactical asset managers, the drawdown in 2018 Q4 did not scare away AIEQ from its portfolio positioning. Some constant large exposures in Alphabet (GOOGL), Amazon (AMZN), Costco (COST), NETAPP Inc. (NTAP), and SS&C Technologies (SSNC)(overall, 10.7% of its portfolio) have contributed to its 2019 recovery (and last years drawdown!) AIEQ maintains a current cash weighting of 3.7%.

What can we learn from how AIEQ weathered the 2018 Q4 drawdown leading into 2019 Q1? First, if you have a strong fundamental basis, there is no reason to run away from your core positioning since they will recover. Certainly, one of its largest holding in Amazon and its -25% drawdown in Q4 could have scared away many active investors; and perhaps causing it to miss its strong 22.3% YTD recovery. Second, there will be periods where you will underperform the market, but over a long horizon you only need to be right 51% of the time to provide an advantage. Third, relatively large and diverse positions can create alpha if you have a firm conviction; for example, AIEQ is currently overweighted to Alphabet (GOOGL) at 3.8% compared to its S&P 500 weighting of 3.0%, thus benefiting from Alphabet's +15.9% YTD index-matching performance. Additionally, broadening the universe to include all market cap sectors provides better diversification exposures. AIEQ includes three mid-cap holdings in its current top 5, being SSNC, NTAP, and Aaron's (AAN).

Quick Take: Trouble with Tactical

I have written a few times over the last few months about the tactical space and how it is a difficult task to call the markets. I follow about 20 tactical asset managers who more or less try to beat the S&P 500. Without getting into names, not one of them has beaten the S&P 500 YTD through April 3, 2019!! Not a one! A couple were close, but why bother with them just to be close when you could simply buy the S&P?

This does not mean that I don’t believe in tactical, since diversifying strategies can be a valid add-on to asset class diversification. It simply means that now is not a time when the tactical models are performing well.

Decomposing High Dividend ETFs (DVY)

I have written a lot about iShares Select Dividend ETF (DVY) over the years and been a long term advocate and holder. I am a fan of the underlying index methodology and still believe it is the best combination of fundamental factors to support long-term growth of principal with a high level of income. However, despite DVY being an ETF with its high level of transparency, it is hard to nail down the sources of return without some sleuthing. Such is the case with today’s huge $0.12 per share increase in the quarterly dividend; from $0.75/share in December to $0.87/share declared today.

On the surface, some of the increase must have come from normal dividend increases on its holdings, but a more interesting source seemed to come from the changes in the portfolio from December to now.

I checked the change in the portfolio from December to now and see a swing in over a $1 billion in low yield holdings into higher yield holdings. Per the table below, DVY sold $1.1 billion of holdings at a 2.00% forward yield (with YTD total return of 11.46%) and bought $1.7 billion of holdings at a 4.15% forward yield (with YTD return of 15.52%).

I cant tell exactly when these transactions occurred, but more than doubling the yield on about 6% of the portfolio during the quarter has a lot to do with the dividend increase. Other things like the unusual low dividend payment in December, timing of dividend payments, and other portfolio rebalancings are also factors.

A Non-Bond Bond Fund

An often overlooked area in the investment universe are closed-end funds (“CEF”). These investment vehicles look and feel like mutual funds and ETFs, but they are “closed.” That is, once they are set up, no new shares are issued (usually) and investors must buy and sell shares on an exchange. Unlike ETFs that are structured to trade on an exchange with “authorized participants” bidding shares close to the net asset value (“NAV”), CEFs have no like structure. In fact, it is unusual for a CEF to trade close to its NAV, with the most often situation being CEFs trading at a discount to NAV.

Many advisory firms manage CEFs that target the bond universe. However, due to the active (some of which are hyper-active) nature, calling these vehicles “bond funds” is a misnomer. Many of these vehicles have risk/return profiles that are equivalent to equity-type investment. One such CEF is the PIMCO Corporate & Income Opportunity Fund (PTY).

Looking at this “bond” fund is an exercise in awe! Its 15-year annual total return ended March 17, 2019 is 13.43%; that blows away the Bloomberg Barclays Aggregate Bond Index of 3.63% and trumps the S&P 500 of 8.57%; but at a bit higher standard deviation risk of 15.32% compared to the S&P 500 risk of 13.58%.

The reason for this is clear. Though PTY is a “bond” fund, it is a “black box” hyper-active bond trading strategy – you are really paying the investment manager (PIMCO) to make all kinds of bets hoping it pays off; any bond-like performance you may see (such as coupon payments) is incidental. The fund is active in derivatives (interest rate swaps) and uses a lot of leverage.

This ultra high risk/return profile has not gone unnoticed in some circles. PTY has historically traded at a relatively high premium to NAV (often in the 20% range) as return seeking investors bid up shares hoping to cash in on its strong historical performance that has continued to defy gravity for 9 of the last 10 years with high top quartile performance. Volatile markets caused the premium to crater in Q4 2018, but it has pushed back up to the 20% range during Q1 2019.

In addition to PTY’s high historical total return performance, the fund has a strong record of paying a flat $0.13 per share distribution every month. This $0.13/share payment equates to a yield of 9.06% at a price of $17.21 (as March 14, 2019). In the case where PTY does not generate enough income to cover the $0.13 distribution, it continues to pay $0.13/share by including a true-up “return of capital” to keep the payment level constant. This is useful to an investor who is using the distributions to cover living expense in retirement and counting of consistency.

Some investors who can afford the relatively high risk profile could benefit from the high level of income and high total return profile. Most of the income is taxed as ordinary income, but the high yield rate makes it still attractive on an after-tax basis.

Tax-Efficient Way to Pay Advisory Fees

There are a few rules of thumb that are worth a lot. A new rule of thumb today is paying investment advisory fees directly out of tax-deferred accounts (IRAs, SEP-IRA, etc.) instead of lumping them together and paying for them from a taxable account. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017 and the revocation of the deductibility of investment expenses, it was a common practice to sweep tax-deferred account advisory fees from a taxable account to get a tax deduction as a miscellaneous expense. However, with the tax law change, it is now almost always more economically advantageous to have tax-deferred accounts pay their own investment expenses.

This idea has been written about on many outlets since the TCJA implementation in 2018, but I still run into situations where old habits die hard and I still see the lumping going on. Michael Kitces, the great thought-leader in the advisory space, has done a good job on this topic and wrote about it on his blog (kitces.com for more detail on this topic). In summary, the payment of advisory fees from a tax-deferred account still retains an implicit tax deduction since the withdrawal to pay the advisory fees is with pre-tax dollars.

For example, for every $1,000 in advisory fees at the 24% tax bracket, there is an implicit deduction of $240. Or, in other words, you can pay $1,000 in fees with only $760 in after-tax dollars. Higher tax brackets and inclusion of state taxes makes the benefit even greater.

An offsetting consideration to this situation includes the idea that leaving assets in a tax-deferred account allows the funds to continue to accrue on a tax-deferred basis. However, despite this being a true statement, the benefits are much less than thought since the tax-deferred earnings are much less than the value of the tax deduction at high marginal tax rates and it takes a very long time horizon to recoup it! Kitces produced a table in his article that demonstrates this.

Additionally, for tax-free Roth accounts, it still makes sense to pay those advisory fees from a taxable account since those funds have the best tax treatment and should be allowed to grow tax free as long as possible.

"Alternative Facts" in Mutual Fund Annual Reports

It’s that time of year again when all the mutual fund companies trot out their annual reports with smiling faces to promote their wares. 2018 was a tough year for most fund companies; especially those with active mandates. According to S&P Versus Active (”SPIVA”) reporting at December 31, 2018 for active large cap mandates, over 5-, 3-, and 1-year horizons 82%, 79% and 64% of active managers underperformed the S&P 500, respectively. It is interesting to see how this fact is communicated to shareholders.

One fund company that I follow seems to report everything with a smiling face when the underlying facts and figures are to the contrary. For example, this is from the Executive Chairman’s letter to shareholders, “…believes active risk management offers downside mitigation and may improve investment outcomes” and “long term perspective” is “ensuring our investment decisions align with the investing time horizons of our clients.” This statement seems to indicate that short term blips in performance are less important than the longer term perspective; so don’t worry about 2018!

When I check the numbers against the text, it doesn’t match up. As we all know, the S&P 500 was down -4.38% in 2018; the fund I am looking at was down -5.31% so it underperformed. We would expect the Executive Chairman to say something to mitigate this -0.93% underperformance in 2018. However, when I look at longer term returns I don’t see much difference. Over 5- or 10-year horizons shown in the annual report we see continued underperformance to the S&P 500 of -1.28% and -1.10%, respectively. These figures are just for “A” class shares (60% of the fund), underperformance is worse for the higher cost shares and better for the lower cost institutional shares.

So, it is hard to see how the Executive Chairman can say something like he did, when the numbers don’t match the words. The “long term perspective” did not help shareholders! Of note, the $5.1 billion mutual fund saw net outflows in 2018 of -$550 million (about 10% of the fund) so someone is noticing. All I can say is “Buyer Beware”!

So You Want to be a Millionaire!

Though most advisers accept that a goal-oriented cash flow approach is the best way to determine your readiness for retirement, some people still look for their “number” – a metric made popular by ING commercials back in 2010. You know, the dollar amount that is saved somewhere that guarantees sunny days and margaritas on the beach during retirement.

Most of the time, this hypothetical “number” is never adjusted for the dreaded “deferred tax liability.” Let’s see how this works and can impact your retirement readiness.

Let’s say you have $1,000,000 saved in two equal buckets; one tax-deferred and one taxable, each with $500,000. Let’s also assume you grew each account by saving $5,000 per year for 25 years and earned a bit over 10% on your investment portfolios.

The benefits of compound interest are immense (see chart), since each account would have unrealized gains equal to about $375,000 on cumulative deposits of $125,000 to total $500,000.

For the taxable account, if we assume a 15% Federal long-term capital gains rate and a 5% state tax rate, the deferred tax liability is simply $375,000 * (0.15+0.05) = $75,000. The trouble gets bigger for the tax-deferred account, since the whole account is taxed at your ordinary income rate. Assuming a 22% tax bracket and a 5% state tax rate the deferred tax liability is $500,000 * (0.22+0.05) = $135,000!

So, you may have $1,000,000, but your total $210,000 deferred tax liability takes a big bite out of the glowing aura! Goal-oriented cash flow investment modeling software does a good job adjusting for this and is a much better way to evaluate your retirement readiness.

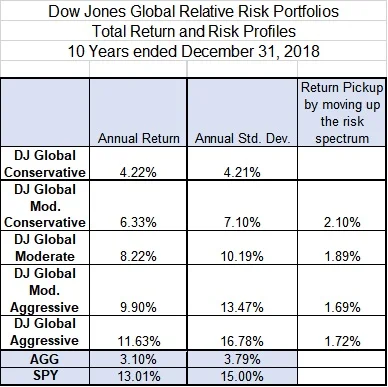

How Much Do You Get Paid For Your Risk?

We all know that more risk usually provides more return, but do we all know by how much? There are many different ways to answer this question with multiple factors to consider. A simple way to look at this is to examine the most recent annualized returns and risk (measured as standard deviation) for a consistently managed diversified portfolio index. One such index is the Dow Jones Relative Risk Portfolio index; specifically, the series that includes global asset classes.

The Dow Jones global indices are structured to provide a smooth exposure to risk with a diversified equity, bond and cash allocation. The Conservative index is structured to provide 20% of the risk of a 100% equity portfolio, the Moderately Conservative index is designed to provide 40%, and so on.

As can be seen from the table, one picked up about 2% in annualized return over the past 10 years ended December 31, 2018 from purely picking one risk tolerance compared to its adjacent neighbor.

So, please take your risk tolerance seriously and make sure it fits with your realistic capacity to bear risk. Factors to consider include your overall wealth, income, and lifestyle; as well as your desire to sleep well at night!

How Good is your Asset Location?

Most pre-retirees and retirees have a combination of taxable, tax-deferred, and tax-free accounts. Different asset classes have different characteristics that make them better candidates for each of these types of accounts.

In general, an asset class that generates a high amount of taxable income, like high yield bonds, bank loans, and emerging market debt, are relatively LESS tax efficient in a taxable account compared to a tax-deferred or tax-free account. Alternatively, an asset class that generates a small amount of taxable income, like U.S. growth stocks, emerging market equities, and commodities, are relatively MORE tax efficient in a taxable account. This is because, of course, assets that don’t generate much taxable income and instead generate most of their return from unrealized gains over time don’t pay taxes until desired and at a preferred lower long-term capital gains tax rate if held more than one year.

I am sometimes surprised when I see a tax-deferred account with a large allocation to some clear long term equity winners like Apple or Amazon. Sure, stocks like these have generated outsized gains over time, but the gains will be taxed at usually higher ordinary income rates when withdrawals are made from the tax-deferred accounts instead of at lower long term capital gains rates. Maybe it is counter-intuitive to some, but stocks like these are better off held in a TAXABLE account to make use of the lower long term capital gains rate, or even the cost basis markup upon bequeath after death!

Vanguard and others have done work defining the benefits of investing with a focus on tax-optimized asset location (“Vanguard Advisor’s Alpha”). It depends on a number of variables, but Vanguard has published that it can be worth from 0 - 75 basis points. It is worth understanding the pros and cons of tax asset location, and then customizing a mix that suits the needs of the investor.

Dividends and Treasury Yields

Dividend-paying stocks have been a great place to be for the past 10 years or so. After the Great Recession in 2008-09, investors looking for yield were forced to look elsewhere from treasury bonds. Treasury bond yields were around the mid-3’s in 2009-10, but quickly fell to the 2% range in 2011 once the Fed’s aggressive quantitative easing (QE) steps took hold as a more proactive force to prop up the weak economy.

The benefit of dividend-paying stocks at that time was clear: earn more than treasury bonds AND have the potential for price appreciation, something that bonds were unlikely to provide given the historic low level in yields. This hand played out very well over the past 10 years as dividend paying stocks, represented by the iShares Select Dividend (DVY) ETF, continuously out-yielded 10-year treasuries AND provided some great price appreciation (see the attached chart for detail). Yes, much more risk trading bonds for equities, but if the need for yield is what drove the investment decision and there was less of a focus or need for price stability, then the investor was aptly compensated.

The question now is, “will this continue?” Can the past 10-years of a “once-in-a-lifetime” scenario continue? Certainly, DVY still has a yield advantage over 10-year treasuries and we are observing a “dovish” Fed currently, so in the near term, “sure”. In fact, tough to see this situation unwind, since if the yield relationship reverses, then there could be a flurry of demand for Treasuries, thus pushing their yields down. We shall see.

Smaller Tax Refund? Big Deal!

The mainstream media is abuzz about the smaller tax refunds being sent out by the IRS this tax season. The New York Times says, “Smaller tax refunds surprise those expecting more relief”, CBS News says, “Americans shocked by impact of new tax law”, while Fox News says, “Smaller tax refunds are a good thing”. Each media outlet has their own spin depending on their agenda, but the real issue is the lack of financial literacy and planning to avoid surprises that could have easily been avoided.

The new tax laws effective for 2018 were well communicated if anyone took the time and energy to understand them; certainly the tax and planning industry was well-versed in the impacts. The elimination of tax deductions due to the $10k limit on state and local taxes (SALT) and the limit on the interest deduction on high value mortgages became a new tax burden for residents in high tax and high property value states. The almost doubling of the standard deduction was intended to lessen that burden, but some high income earners with large SALT and mortgage interest were sure to see an increase. So, taking the lowered payroll withholdings due to the lowered tax brackets was a flawed assumption if you ignored the loss of those large deductions in your tax planning.

Alternatively, if you were NOT a high income earner, your total Fed taxes likely went DOWN, but you simply got a smaller tax refund because you took a portion of your end-of-year refund in smaller bits during the year due to the lower withholding amounts. Effective planning could have easily avoided this “surprise”. Moreover, consistent with the Fox News article, a Treasury spokesperson said in a statement, “Smaller refunds mean that people are withholding appropriately based on their tax liability, which is positive news for taxpayers.” Unfortunately, this seems to have happened to some taxpayers due to inaction and ignorance instead of through conscious planning.

Keeping more of your money during the year with an effective saving and investing strategy makes much more sense than giving the government an interest-free loan during the year. Hopefully, this kind of event will cause a more focused interest in financial education and planning.

"V" gets a Vote of Confidence!

“Buy the Dip” appears to be alive and well! After the abysmal October leading into the horrid December, things have recovered quite nicely! From the recent plateau on December 3, 2018, the S&P 500 (per the ETF, SPY) is only 0.77% off that level per the above chart. Not a pure “V”, but pretty close!

Though the mainstream media does a good job pitching its dire Koolaid to drive ratings and eyeballs, the doomsayers have not been too accurate thus far. On these pages, I have commented on weaknesses in the predictive ability of a yield curve inversion to forecast a recession, identified underlying strength through the important PMI (Purchasing Mangers Index) levels, talked about positive technical factors such as seasonal rebalancing into equities after the large Q4 and December drawdowns to get back to equity targets, and highlighted some well-thought out (and positively-leaning) forecasts from Northern Trust Asset Management and my prior firm, Sun Life Financial.

It is a very rare situation, indeed, where it would be prudent to rebalance away from a strategic allocation to “risk” assets. The situation through December indicated a reasonable case to be cautious, but not fearful, while waiting for some key economic statistics to show their hand. Happily, hanging onto your hat and weathering the storm appears to have paid off this time - for now.